| Join Telegram |  |

| Join Whatsapp Groups |  |

Atal Pension Yojana | APY Scheme Details, Eligibility, Benefits, Application Form: Atal Pension Yojana is a Government pension scheme for the unorganized sectors of India. This scheme was launched by the Prime Minister of India in the year 2015. Pension Fund Regulatory and Development Authority (PFRDA) is the government body that administers the APY under the National Pension Scheme Architecture. The objective under providing this scheme is to ensure that no one in India should worry about the illness, accidents, diseases in old age, giving a sense of security. Under the APY, guaranteed minimum pension of Rs. 1,000/- or 2,000/- or 3,000/- or 4,000 or 5,000/- per month will be given at the age of 60 years depending on the contributions by the subscribers. In the below sections we have provided you the required information regarding Atal Pension Yojana (APY).

Atal Pension Yojana Scheme – Overview

| Name of the Scheme | Atal Pension Yojana (APY) |

| Administered by | Pension Fund Regulatory and Development Authority (PFRDA) |

| Objective | To provide pension |

| Population covered | Unorganized sector |

| Status | Active |

| PFRDA Official site | pfrda.org.in |

Atal Pension Yojana (APY) Eligibility

- Candidate must be the native member of India,

- Must be aged between 18-40 years.

- Should make contributions for a minimum of 20 years.

- The applicant must have a bank account linked with your Aadhar.

- Must have a valid mobile number.

Benefits of APY Scheme

- Under APY Scheme The pension is guaranteed by the Government of India.

- The applicant of APY gets a guaranteed pension of Rs.1000/- to Rs.5000/- per month.

- The tax benefits under this APY scheme are the same as applicable under NPS (National Payment Scheme).

- APY Scheme is not only beneficial for the applicant, but also for his /her spouse. In case of death of the applicant the spouse will be entitled to the pension. In case of the demise of both applicant and spouse, the nominee will be entitled to get the same pension.

- APY Scheme is also beneficial as the government also co-contribute Rs.1000/- per year or 50% of the total contribution whichever is low.

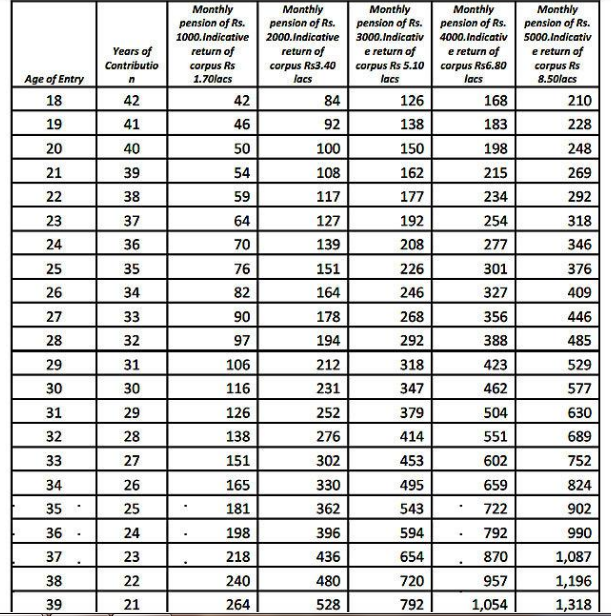

APY Monthly Contribution

Withdrawal Procedure From APY

The APY account can be withdrawn in the following conditions.

On attaining the age of 60:- Upon completion of 60 years, the subscribers will submit the request to the associated bank for drawing the guaranteed minimum monthly pension or higher monthly pension, if investment returns are higher than the guaranteed returns embedded in APY. The same amount of monthly pension is payable to the spouse (default nominee) upon the death of the subscriber. The nominee will be eligible for the return of pension wealth accumulated till age 60 of the subscriber upon the death of both the subscriber and spouse.

In case of death of the subscriber due to any cause after the age of 60:- In case of death of the subscriber, the same pension would be available to the spouse and on the death of both of them (subscriber and spouse), the pension wealth accumulated till age 60 of the subscriber would be returned to the nominee.

Exit before the age of 60:– In case a subscriber, who has availed Government co-contribution under APY, chooses to voluntarily exit APY at a future date, he shall only be refunded the contributions made by him to APY, along with the net actual accrued income earned on his contributions (after deducting the account maintenance charges). The Government co-contribution, and the accrued income earned on the Government co-contribution, shall not be returned to such subscribers.

Death of subscriber before age of 60:- In case of death of the subscriber before 60 years, the option will be available to the spouse of the subscriber to continue contributing in the APY account of the subscriber, which can be maintained in the spouse’s name, for the remaining vesting period, till the original subscriber would have attained the age of 60 years. The spouse of the subscriber shall be entitled to receive the same pension amount as the subscriber until the death of the spouse. Or, the entire accumulated corpus under APY will be returned to the spouse/nominee.

Atal Pension Yojana Penalty for Default

The savings account under APY will be considered default if sufficient balance will not be maintained for contribution on the due date.

The bank will be charged an extra amount for delayed payments as shown in below.

- One rupee per month for the contribution up to Rs.100/- per month.

- Two rupees per month for contribution in between Rs.101 to 500/- per month.

- Five rupees per month for the contribution between Rs.501/- to Rs.1000/- per month.

- Rs.10/- per month for contribution more than Rs.1001/- per month.

Atal Pension Yojana (APY) Discontinuation of payment

Candidate must ensure that their APY account is funded enough for auto-debit of contribution amount. Otherwise, the applicant will face following issues.

- After 6 months, APY account will freeze.

- After 12 months, APY account will deactivate.

- And After 12 months, APY account will close.

Atal Pension Yojana App

Atal Pension Yojana App has been introduced by PFRDA to enable easy access to APY accounts for subscribers. By installing the app, you can check your APY account balance, details of when the next contribution is due, APY account details, APY transactions list, and more. The Atal Pension Yojana App from PFRDA is available for free from the Android App Store.

Other Important Facts About APY

- It is mandatory to provide nominee details in the APY account. If the applicant is married, the spouse will be the default nominee. The unmarried applicant can nominate any other person as nominee & they have to provide spouse details after marriage. The Aadhaar details of spouse and nominees may be provided.

- Candidate can open only one APY account and it is unique. Multiple accounts are not permitted.

- Aspirant can opt to decrease or increase pension amount during the course of accumulation phase, once a year.

- The periodical information to the applicant regarding activation of PRAN, balance in the account, contribution credits, etc. will be intimated to APY applicant by way of SMS alerts. The applicant will also be receiving the physical statement of Account once a year.

- The physical statement of APY will be provided to the applicant annually.

- The contribution may be remitted through auto-debit uninterruptedly even in case of change of residence/location.

- The scheme is open for Indian citizens only.

- The APY applicant can change the mode (monthly/quarterly/half-yearly) of the auto-debit facility once in a year during the month of April.

How To Open Atal Pension Yojana Account?

- Approach the bank branch/post office where an individual’s savings bank account is held or open a savings account if the subscriber doesn’t have one.

- Provide the Bank A/c number/ Post office savings bank account number and with the help of the Bank staff, fill up the APY registration form.

- Provide Aadhaar/Mobile Number. This is not mandatory, but may be provided to facilitate the communication regarding contribution.

- Ensure keeping the required balance in the savings bank account/post office savings bank account for the transfer of monthly/ quarterly/ half-yearly contribution.

APY – Important Link

To know more details about Atal Pension Yojana (APY) Scheme & Apply Link – Click Here

If you want to get more updates on Atal Pension Yojana (APY), then you can bookmark our website Freshers Now by pressing Ctrl+D.